Does Workers' Comp Cover Independent Contractors? A Guide for Companies That Hire 1099s

A standard workers' compensation policy does not cover independent contractors as contractors. Workers' comp is built around the employer-employee relationship, so the only way your policy reaches a 1099 worker is by treating that worker as your employee. That's the classification issue most companies hire contractors to avoid.

If a broker or carrier tells you your policy "covers" your contractors, they usually mean something more specific: if a contractor is later found to have been your employee, the policy may respond to the claim and your carrier will charge the corresponding premium at audit. That's different from saying an independent contractor is covered as an independent contractor.

The distinction matters because workers' comp is only one part of the picture. How a carrier treats your contractors affects premium audits, misclassification risk, and what happens when a contractor is injured. This guide explains why companies are often told their contractors are "covered," what that actually means in practice, and why coverage held in the contractor's own name avoids the contradiction.

"My broker says my policy already covers them"

Many companies are told some version of "your policy already covers your contractors." The confusion usually comes from using the word covered to describe different kinds of insurance.

A broker may explain that your general liability policy extends to work performed by your contractors. That's referring to vicarious liability: protection for your company if a contractor causes injury or property damage to someone else while performing work on your behalf. It is not workers' compensation for the contractor's own injury.

The same ambiguity shows up with workers' comp. When someone says your contractors are "covered," what they often mean is that if a contractor is injured, claims they were really your employee, and that claim succeeds, your workers' comp policy may respond. Your carrier then treats that worker as your employee for premium purposes and bills the additional premium at audit.

That's a safety net for your company's potential liability. It is not workers' comp coverage for an independent contractor as an independent contractor.

The distinction matters because those are two very different positions. One says, "This person is an independent business that carries its own risk." The other says, "If necessary, we'll treat this person as your employee." Those positions cannot both be true at the same time.

What state statutes actually say about 1099 contractors

Workers' compensation laws vary by state, but the underlying principle is remarkably consistent: workers' comp exists to cover employees, not independent contractors. Florida provides one of the clearest examples.

Under Section 440.10, a covered employer "shall be liable for, and shall secure, the payment to his or her employees" of the benefits provided under the statute. The obligation runs from employer to employee.

The statute then defines who qualifies as an employee. Section 440.02 expressly excludes "an independent contractor who is not engaged in the construction industry." Construction is a notable exception because many states have adopted special statutory employee rules for that industry. Outside those exceptions, a genuine independent contractor generally falls outside the employer's workers' compensation policy.

Florida isn't unusual in this respect. Although the details differ from state to state, workers' compensation systems are built around the employer-employee relationship. That's why the recurring claim that an employer's policy "covers independent contractors" deserves scrutiny. If the worker remains an independent contractor, the policy generally does not apply. If the policy does apply, it's typically because the worker is being treated as an employee.

The two problems: the coverage gap and the misclassification signal

If your contractors are genuinely independent, your workers' compensation policy generally doesn't cover them. That's the first problem.

When an uninsured contractor is seriously injured, they have no workers' comp remedy of their own. If they believe they were functioning as an employee, their strongest path to recovery is often to argue exactly that. The classification question that seemed theoretical during onboarding becomes the central issue after an injury.

If a court, workers' compensation board, or other authority ultimately concludes the worker should have been treated as your employee, the consequences extend beyond the claim itself. Depending on the circumstances, the company may face retroactive premium assessments, payroll tax exposure, employment-law liability, and state-specific penalties for failing to maintain required coverage. In Colorado, for example, the Division of Workers' Compensation can assess penalties of up to $500 per day against employers that fail to carry required coverage. Oklahoma authorizes penalties of up to $1,000 per day under its workers' compensation statute.

It's natural to look for an alternative that protects contractors without treating them as employees. Occupational accident insurance is often presented as that solution, but it serves a different purpose. Unlike statutory workers' compensation, occupational accident policies typically provide scheduled benefits with defined limits. Medical expenses, disability payments, and death benefits are capped by the policy rather than determined by statute.

That difference matters because workers' compensation is built on a tradeoff. Employees receive statutory benefits without proving fault, and in exchange generally lose the right to sue their employer for workplace injuries. Lawyers refer to this protection as the exclusive remedy doctrine. Alternative policies generally don't provide the same protection. If their benefits are exhausted, an injured worker may still pursue a negligence claim against the hiring company. California's workers' compensation statute illustrates this principle in Labor Code Sections 3600 and 3602. North Carolina and Texas have likewise made clear that occupational accident coverage is not a substitute where workers' compensation is legally required.

There's also a practical issue that often surprises companies. During a premium audit, carriers generally do not treat occupational accident coverage as proof of workers' compensation. If a contractor cannot demonstrate qualifying workers' comp coverage, their payments may still be included in your payroll calculations and generate additional premium. In other words, you've purchased a policy that may provide some benefits after an injury while leaving both the audit exposure and the potential lawsuit intact.

Those are the consequences of the coverage gap. The second issue is more subtle: what it signals when a company says its workers' compensation policy "covers" its contractors.

Workers' compensation is designed for employees. If coverage exists only because the contractor is being treated as an employee, that treatment points in the opposite direction from the independent-contractor relationship the company is trying to establish. Classification disputes consider many factors, and insurance alone is never determinative, but voluntarily insuring a worker under an employee policy is rarely evidence you'd want to explain later.

The stakes are substantial. New York's attorney general recovered $328 million from two rideshare companies over how they classified and paid drivers, and other high-profile misclassification settlements have reached into the hundreds of millions of dollars.

One practical way to understand how carriers view the issue is to ask for a quote that explicitly covers your contractors under your own workers' compensation policy. The premium typically increases dramatically because the carrier prices those workers as employees on your payroll. That pricing reflects the same principle discussed throughout this guide: the policy works by treating the contractor as an employee, not as an independent business.

What a premium audit does to uninsured contractor pay

A workers' compensation policy isn't a flat-fee product. At the beginning of the policy term, your carrier estimates your payroll and calculates an initial premium. At the end of the policy period, it performs a premium audit to determine the actual exposure it insured.

For companies that hire independent contractors, one question often drives the outcome of that audit:

Did each contractor maintain valid workers' compensation coverage while performing the work?

To answer that question, the auditor reviews contractor payments and requests proof of coverage. If you can't produce a valid certificate of insurance showing the contractor maintained workers' compensation during the period they worked, the auditor may treat those payments as employee payroll and charge additional premium.

This is why companies are often surprised by their audit results. The issue isn't whether the contractor received a Form 1099 or signed an independent contractor agreement. The audit focuses on whether the contractor carried qualifying workers' compensation coverage during the work being audited.

The financial impact can be significant. One business owner described an estimated premium of roughly $8,000 that increased to more than $40,000 after payments to uninsured contractors were included in the payroll calculation. Another reported receiving an audit adjustment exceeding $90,000 after a large roster of uninsured contractors was reclassified.

For companies that rely on contractor labor, this is one of the most common sources of unexpected workers' compensation costs—and one of the least understood parts of the premium audit process.

When an uninsured contractor's injury becomes your problem

A premium audit isn't the only time uninsured contractors create risk. The more difficult situation is when someone gets hurt.

If a contractor you hired is injured while performing work and doesn't have workers' compensation coverage of their own, they have no workers' comp remedy available as an independent contractor. Depending on the facts, they may argue they were actually your employee or pursue a negligence claim outside the workers' compensation system.

Either path shifts the focus to your relationship with the worker. Questions that may have seemed routine during onboarding—how much control you exercised, how the work was performed, whether the contractor operated an independent business—can become central to determining who bears responsibility for the injury.

This is why verifying coverage before work begins matters so much. Once an injury occurs, your options become limited. You're no longer deciding how to manage risk—you are responding to a claim that has already been filed.

Why you can't just add contractors to your own policy

A common reaction to the coverage gap is straightforward: Why not simply add contractors to the company's workers' compensation policy?

The difficulty is that workers' compensation is an employee benefit. If a company voluntarily places an independent contractor under a policy designed for employees, it becomes harder to explain why that same worker should be treated as an independent business for classification purposes.

Insurance is only one factor in a classification analysis, and it isn't determinative on its own. Courts and agencies look at the entire relationship between the parties, including the degree of control exercised over the work. But voluntarily insuring a worker under an employee policy is rarely evidence that supports an independent-contractor relationship.

That leaves companies in an uncomfortable position. If contractors carry no workers' compensation coverage, an injury can lead to disputes over classification and premium audits may result in additional charges. If the company instead provides workers' compensation under its own employee policy, it may undercut the independent-contractor relationship it intended to establish.

The cleaner approach is for the contractor to maintain statutory workers' compensation coverage as their own business. The contractor remains the insured, the employer's policy remains limited to employees, and the two insurance relationships stay consistent with the underlying business relationship.

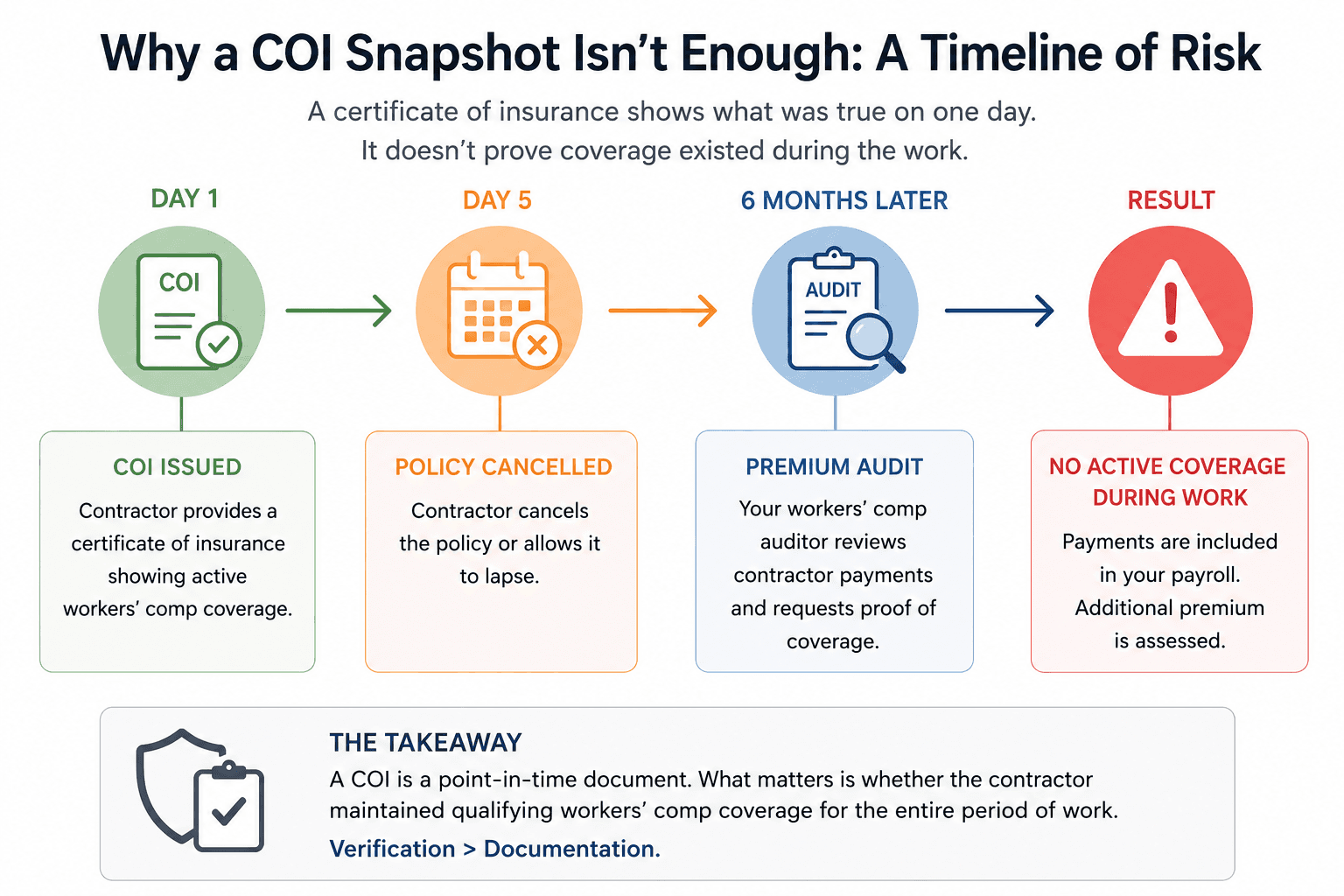

The trouble with COIs, ghost policies, and expired coverage

For many companies, collecting a certificate of insurance (COI) is the standard way to verify contractor coverage. The problem is that a certificate only shows what was true on the day it was issued. It is not proof that coverage remained in force throughout the work.

A contractor can present a valid certificate to satisfy your onboarding process and later allow the policy to lapse or cancel it altogether. By the time your workers' compensation audit occurs months later, the certificate no longer reflects the coverage that existed during the period being audited. If the contractor cannot demonstrate they maintained qualifying workers' compensation coverage while performing the work, the auditor may still include those payments in your payroll calculations.

There's a second issue that's less widely understood: the ghost policy.

In some states, sole proprietors with no employees are allowed to exclude themselves from workers' compensation coverage. Some purchase a policy solely to obtain a certificate of insurance, while excluding the only person performing the work. The result is a policy that generates a valid-looking COI but provides little or no protection if that contractor is injured.

From an audit perspective, a ghost policy may satisfy a paperwork requirement in some circumstances, but it doesn't change the underlying reality that the contractor may not have had meaningful workers' compensation protection. One contractor described paying roughly $2,500 in additional premium after solo contractors presented this type of policy. More importantly, if the contractor is injured, the certificate itself doesn't pay the claim.

A certificate of insurance is an important document, but it's only as valuable as the coverage standing behind it. Verifying that coverage remained active during the work matters far more than collecting a certificate once during onboarding.

What contractor-held coverage fixes

Coverage held in the contractor's own name keeps the insurance relationship consistent with the business relationship. The contractor remains the insured, the hiring company continues to insure only its employees, and the workers' compensation system operates as it was designed.

That consistency addresses both issues discussed throughout this guide.

From an audit perspective, the contractor carries their own qualifying workers' compensation coverage, giving the auditor evidence that the exposure belonged to the contractor rather than the hiring company. Assuming the coverage remained valid during the work, the contractor's payments generally aren't swept into the employer's payroll calculation.

It also supports the underlying contractor relationship. Insurance alone never determines worker classification, but a business that carries its own statutory workers' compensation coverage is assuming responsibility for its own workforce rather than relying on the hiring company's employee policy.

There's another important consequence: exclusive remedy.

When an injured worker is covered by statutory workers' compensation, the claim is generally handled within that system. In exchange for receiving no-fault benefits, the worker's ability to bring a negligence lawsuit against the responsible employer is generally limited. That's one of the core features of workers' compensation law.

Without statutory workers' compensation, that protection may not exist. An occupational accident policy may pay benefits, but it doesn't necessarily replace the legal protections that accompany workers' compensation. Depending on the facts and applicable law, an injured contractor may still pursue a negligence claim if those benefits don't fully compensate their losses.

Historically, maintaining statutory workers' compensation hasn't been practical for many independent contractors. Traditional annual policies often require substantial upfront premiums and year-long commitments that don't fit short-term or project-based work. As a result, many contractors simply go without coverage.

Per-assignment workers' compensation was developed to address that problem. Instead of requiring a year-long policy, coverage is issued in the contractor's own name for a specific engagement, making statutory workers' compensation practical for short-duration work while preserving the separation between the hiring company's policy and the contractor's own business.

1099Policy follows this model by issuing workers' compensation in the contractor's own name on a per-assignment basis. For companies that rely on contractor labor, the result is a structure that's consistent with both the workers' compensation system and the underlying independent-contractor relationship.

Frequently asked questions

Do independent contractors need to be covered under my workers' compensation policy?

Generally, no. Workers' compensation policies are designed to cover employees, not independent contractors. If a contractor doesn't maintain their own qualifying workers' compensation coverage, however, your carrier may treat their payments as employee payroll during a premium audit and assess additional premium.

My broker says my policy already covers my contractors. Is that true?

It depends on what "covered" means. A workers' compensation policy may respond if a contractor is later determined to have been your employee, but that's different from providing coverage for an independent contractor as an independent contractor. General liability policies can also cover your company's liability for a contractor's work, which is a separate type of protection.

What happens during a workers' compensation premium audit?

At the end of the policy period, your carrier reviews the exposure it actually insured. For companies using independent contractors, auditors typically request proof that contractors maintained qualifying workers' compensation coverage while performing the work. Without that documentation, contractor payments may be included in your payroll calculations, increasing your premium.

What is a ghost policy?

A ghost policy is a workers' compensation policy purchased primarily to generate a certificate of insurance, often by a sole proprietor who has excluded themselves from coverage where state law allows. While it may produce a valid certificate, it may provide little or no protection if the contractor performing the work is injured.

Does occupational accident insurance replace workers' compensation?

Generally, no. Occupational accident insurance is a private insurance product with scheduled benefit limits. It does not automatically provide the statutory protections associated with workers' compensation, including the exclusive remedy framework that often limits workplace injury lawsuits.

If I insure my contractors under my own workers' compensation policy, does that make them employees?

Not by itself. Worker classification depends on the entire relationship between the parties, including factors such as control over the work. However, voluntarily insuring a contractor under a policy intended for employees may be difficult to reconcile with the position that the worker is operating as an independent business.

Why is contractor-held workers' compensation different?

When workers' compensation is issued in the contractor's own name, the insurance structure matches the business relationship. The contractor remains responsible for their own coverage, the hiring company's policy remains limited to employees, and the contractor's payments generally aren't treated as uninsured payroll during a premium audit, assuming qualifying coverage is maintained.